Comparing HSAs, HRAs and FSAs: Which Approach Is Best?

Employers are increasingly looking to consumer driven health plans as part of their employee benefits strategy to help soften the blow of continually rising health care costs. Depending on the model, consumer driven health plans typically include health reimbursement arrangements (HRAs), flexible spending accounts (FSAs) or health savings accounts (HSAs).

Consumer driven health plans generally increase employees’ stake in their own health care costs. In most cases, a consumer driven health plan covers a wide range of medical expenses, but also includes more cost-sharing for participants (for example, higher deductibles). Some plans incorporate an HRA, health FSA or HSA to help employees pay for their out-of-pocket medical expenses on a tax-free basis. This article provides some basic information about the similarities and differences between HRAs, FSAs and HSAs.

Health Savings Accounts (HSAs)

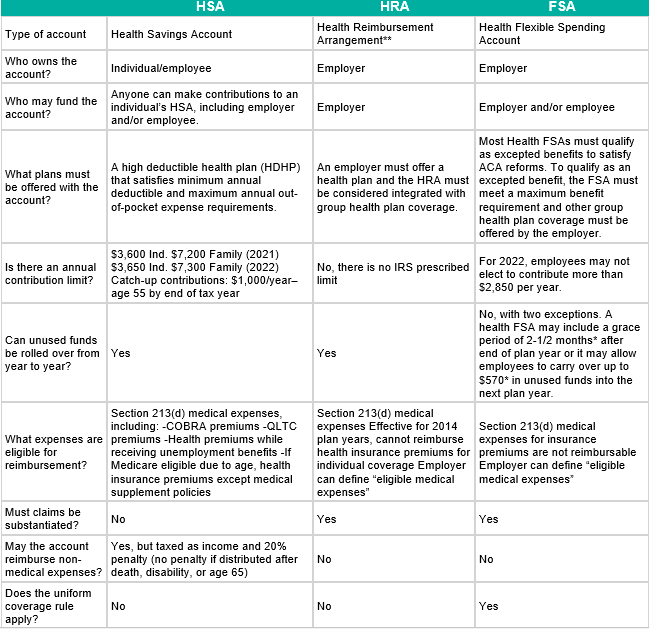

Due to their tax-favored status, HSAs have strict rules regarding eligibility and contributions. In order to make or receive HSA contributions, individuals must meet the following qualifications:

- Be covered by a high deductible health plan (HDHP)

- Not have any other health coverage (with some exceptions)

- Not be claimed as a dependent on another person’s tax return

- Not be covered by Medicare

The employer and employee can contribute to the HSA in the same year, subject to annual limits. Employers may allow employees to make pre-tax salary reduction contributions to fund their HSAs. Individuals may roll over unspent funds in the HSA from year to year. Since the HSA is a tax-exempt account owned by the employee, he or she may keep the account upon termination of employment or retirement.

Health Flexible Spending Accounts (FSAs)

Health FSAs provide a means for employees to reduce their income tax liability through salary reduction. Employees can contribute a portion of their own salary to an account designated to pay for health care expenses. These pre-tax contributions are exempt from income and payroll taxes. The Affordable Care Act (ACA) limits employee’s pre-tax contributions to their health FSAs to $2,850 (adjusted for inflation for future plan years).

There are some strict design requirements for health FSAs that have negatively impacted their popularity. While any individual who satisfies the HSA eligibility criteria can make HSA contributions, only employees can participate in a health FSA. This means that, while self-employed individuals can establish health FSAs for their employees, they cannot set up their own a

In addition, FSAs have a “use-it-or-lose-it” provision. In general, employees are required to elect a specific amount of salary reduction at the beginning of the year, and then must use every dollar in the account by the end of that year. Because annual medical expenses are hard to predict, employees often overfund the accounts and then spend unnecessarily at the end of the year to avoid forfeiting the money in their accounts.

To help avoid this problem, the IRS allows health FSAs to incorporate either a grace period or carry-over feature. Health FSAs with a grace period allow participants to access unused amounts remaining in an FSA at the end of the plan year to pay for expenses incurred during a grace period of up to two and a half months after the end of the plan year. Alternatively, health FSAs may allow participants to carry over up to $570* of unused funds remaining at the end of a plan year to be used for qualified medical expenses incurred during the following plan year.

Health FSAs are also subject to a uniform coverage rule, which requires the health FSA to operate like an insurance plan, with the employer assuming the risk of loss. Under this rule, an employee’s maximum reimbursement amount for a year must be available at any time during the coverage period, even if a reimbursement would exceed the year-to-date contributions to the employee’s FSA.

Health FSAs are group health plans that are subject to laws such as the ACA, the Health Insurance Portability and Accountability Act (HIPAA) and the Consolidated Omnibus Budget Reconciliation Act (COBRA).

Health Reimbursement Arrangements (HRAs)

HRAs allow employees to use employer contributions to pay for (or reimburse) eligible medical care expenses. HRAs can only be funded with employer money; employees cannot make contributions to their HRAs. Unlike health FSAs, unused HRA balances may accumulate from year to year.

There is no specified cap on the amount an employer is allowed to contribute to an HRA. Also, an HRA is not subject to the uniform coverage rule that applies to health FSAs. However, like health FSAs, only employees can participate in an HRA, which means that self-employed individuals cannot participate in an HRA on a tax-favored basis.

Like health FSAs, HRAs are group health plans that are subject to laws such as HIPAA and COBRA. Under the ACA, most HRAs must be “integrated” with another group health plan to satisfy certain market reforms. However, there are exceptions to this requirement for certain types of HRA designs, including retiree-only HRAs.

Deciding on the Right Approach

Introducing consumerism into your health plan requires an evaluation of the benefits and disadvantages of HSAs, FSAs and HRAs. No one solution is right for every employer. If your organization is considering implementing a consumer driven health plan, your Exude, Inc. representative can help you decide which plan is best for you.

You may also like

-

![]() Jenna Conroy / January 23, 2025

Jenna Conroy / January 23, 2025 -

![]() Jenna Conroy / October 30, 2024

Jenna Conroy / October 30, 2024 -

Signup for our stories

Fresh thinking delivered to your inbox once a month.